America runs on credit. Odds are, when you step foot in a car dealership you’ll need to be prepared to fill out a form or two that let the dealer check your credit score. However, many people don’t know what credit score car dealers actually use.

Unlike your traditional FICO score, car dealers — more accurately lending institutions that sell auto loans to dealerships — refer to another, less known score, called The FICO® 8 Auto Score, or its competitor CreditVision. To answer the question “What credit score do car dealers use?” We need to learn more about both of these products.

What is FICO® 8 Auto Score?

Fair Isaac Corporation (FICO) is a publicly traded data analytics company. You’re most likely familiar with their FICO score. Your FICO score is a representation of your credit worthiness.

FICO offers specific products and solutions for car dealers and auto loans. Their product is called Auto Score 8. As you can see here from FICO’s promotional materials, Auto Score 8 is meant to help dealers, “Improve accuracy and speed of decision making. Increase your automatic approval rate with better customer knowledge, the most proven and predictive credit-risk scores, and a holistic understanding of the customer relationship over time.” To answer the question ‘What credit score do car dealers use?” We need to dig into Auto Score 8, as it is in the industry standard credit score for auto loans.

Similar to your normal FICO score, you can request a copy of your current Auto Score from FICO for a fee.

What you really need to understand is that your Auto Score is calculated similarly, but differently than your traditional FICO score. The score range for the Auto Score is 250-900 (instead of the traditional 300-850). FICO promotes that Auto Score will help dealerships and lending institutions in five distinct ways:

- Increase regulatory compliance. With today’s shifting compliance landscape and the need to be more agile, it is more important than ever to have proper governance as well as explainability and fast auditability of all decisions made.

- Aggressively compete & meet portfolio objectives. FICO technology enables you to leverage machine learning and analytics to achieve your desired business outcomes and deliver highly compelling and personalized offers.

- Improve accuracy and speed of decision making. Increase your automatic approval rate with better customer knowledge, the most proven and predictive credit-risk scores, and a holistic understanding of the customer relationship over time.

- Combat financial crime. FICO can protect your business against emerging threats like synthetic fraud, traditional 1st and 3rd party fraud, and enterprise data breaches using artificial intelligence and machine learning.

- Improve customer and dealer loyalty. Today’s customer demands digital and multi-channel personalized engagement as well as a holistic view of their customer experience over time. Today’s auto dealers need complementary tools that enable them to better partner with you. Create value for everyone involved with the FICO platform.

What is CreditVision?

FICO does not have a monopoly on the credit score market. There are other data analytics companies out there that want a slice of the pie.

TransUnion offers a product called CreditVision, which competes directly with FICO. Although CreditVision is not specific to car dealers or auto loans, it is important to mention here. When it comes to understanding what credit score car dealers use, CreditVision is important to be aware of.

TransUnion does offer dealer specific solutions that you should be aware of. This 2018 marketing video helps you get an understanding of what they provide dealerships with.

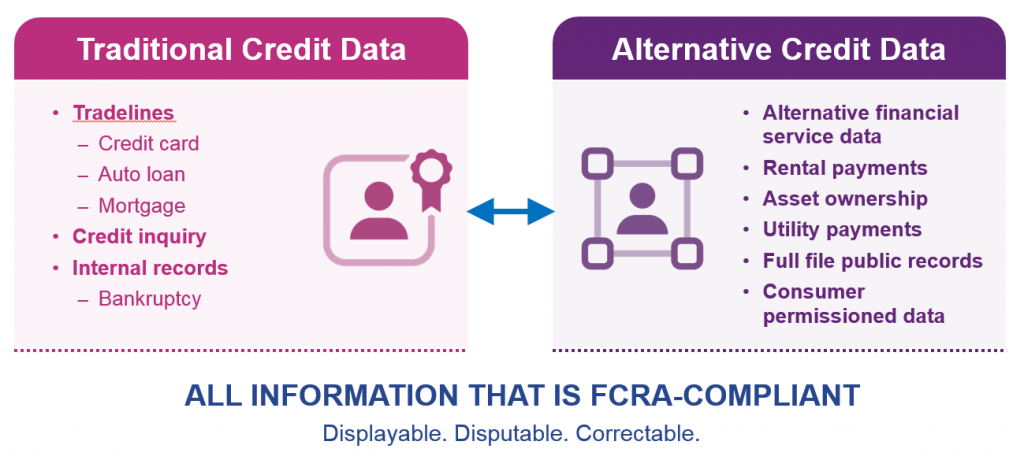

The main draw of CreditVision is the products ability to look at alternative credit data when calculating your score. Alternative credit data can include:

- Rental payments;

- Utility payments;

- Cell phone payments;

- Asset ownership;

- Etc.

3 things that impact your credit score

Regardless of if a dealership is using FICO® 8 Auto Score or CreditVision, my experience has taught me that there are three things that the banks and credit unions look at to determine your creditworthiness. They are, ability, stability and willingness.

Ability

Ability is defined by how much you earn and how much you payout on a monthly basis. In other words, do you have the ability based on your income to direct a certain percentage of that towards things like housing costs (mortgage or rent payments), car loans, and credit card payments?

Banks usually don’t want your debt payments to exceed more than 35 to 40% of your gross income. Say you earn $5,000 gross a month before taxes and deductions. The maximum amount of money banks would want to see you spending on debt is $2,000 per month.

This includes housing, cars and credit cards.

When you go to the dealer, ask yourself, “Do I have the ability, based off of what I earn and my current obligations, to take on additional debt?” That’s the question the dealer is asking themselves!

Stability

Stability is how long you have lived where you live, how long you have worked where you work, how long you’ve been employed in your line of work, and many other things of that nature.

Have you had three different addresses and four different jobs in the last three years? If you have, that would not show a bank stability. If you’re constantly moving and you’re having difficulty keeping a job for an extended period of time that could be a “red flag.”

Stability for the bank is someone who has resided at the same address for three years or longer, has been employed by the same employer for three years or longer, or has been employed in the same field for an even longer period of time.

Perhaps you’re a real estate agent and you’ve been in that line of work for 10 years. You’ve been with your present employer for three years, and you’ve lived at your current address for five years. That to a tee is stability.

You don’t move a lot, and you’ve been working in your industry for 10 years. To a car dealer or a bank, you don’t represent a big risk. If you have stability, you’re potentially the type of customer they are looking for, but that all depends on the last factor; willingness.

Willingness

Willingness, is how you have handled your past debt obligations; mortgages, car loans, credit cards, phone bills and the like.

Have you paid them on time all the time or just some of the time? Have you paid them off ahead of schedule or did you fall behind schedule? If you fell behind schedule, how often did that happen? Did it happen once in three years or did it happen a dozen times in those three years?

Willingness signals to the bank exactly what kind of risk your loan poses to them.

If all of your accounts have always been paid on time or early, you are more than likely to get a loan quickly and easily because you pose little risk to the bank. If however you have a track record of paying your obligations off late, you immediately become riskier for the bank.

This generally translates into paying a higher interest rate. If the dealer or the bank is going to take the risk, they want to make money off of it. The greater the risk (less willing you’ve been in the past) the higher your rate of interest.

What credit score do you need to lease a car?

If you’re thinking about leasing or buying a car, you might enjoy this article if you haven’t read it already: How Much Do Dealers Markup Used Cars?

Now that we’ve answered the question “What credit score do car dealers use?” And we’ve addressed the three factors that influence your credit score, let’s discuss what credit score you actually need to buy or lease a new car.

In order to lease a car, you need to convince the leasing company that you’ll be able to make your monthly payments for the full time period of the lease. Unlike when you buy a car, leasing entails no ownership responsibility. In that regard, leasing is similar to renting an apartment. Each month the landlord expects payment. The same goes for your car lease.

620 is a minimum score you need to secure a lease. Below that, when you reach subprime credit, your chances of convincing a leasing company to “rent” you a vehicle become very challenging. This isn’t to say it’s impossible, however it certainly won’t be at an attractive price point.

A credit score in the Prime range will yield more favorable terms.

What credit score do you need to buy a car?

Unlike leasing, when you buy a car you become the individual holding the title. It’s relatively rare that someone comes into a dealership with cash and pays for a car upfront. With interest rates as low as they are, it really makes no sense why anyone would do that.

That means you’ll be financing your car. Nearly anyone can receive a loan on a car. The challenge will be getting the best rate possible. As your credit score decreases, the loan interest rate increases.

Dealers and banks charge you a higher interest rate if your credit score is low because you pose a greater risk to default (not pay the loan back). This is how dealers and banks “diversify” the risk in their portfolio. They charge really high rates to people who generally can’t really afford them, and really low rates to those that can. It doesn’t necessarily make sense from the consumer standpoint, but for the dealers it does.

| Credit score range | New car loan | Used car loan |

| Super prime: 781 to 850 | 4.19% | 4.69% |

| Prime: 661 to 780 | 5.01% | 6.38% |

| Nonprime: 601 to 660 | 7.91% | 10.91% |

| Subprime: 501 to 600 | 12.17% | 16.78% |

| Deep subprime: 300 to 500 | 14.88% | 19.62% |

What is the moral of the story? If you want to get a car loan with little to no hassle, you need to always pay your loans, utility bills and credit cards on time. By doing this you will assure yourself the continued availability of credit at the best and least expensive rates and terms.

So always remember that banks are looking for your ability to repay your loan, the stability you have shown in your career and how often you have moved and how willingly you have paid back your past credit obligations. Ability, stability and willingness. These are the keys to good credit.

0 Comments