If you’ve noticed things getting a bit hectic lately, you’re not alone. Two years into the pandemic, 2022 has brought its own set of challenges, setbacks and surprises. Maybe you’ve been impacted by one of these challenges, or perhaps you’re one of the fortunate few who haven’t. Here at CarEdge we’ve been asking ourselves “what happens in 2022 and beyond” to help us plan for our business. Today I thought we would share our thoughts with you.

We’re entering a recession and will stay there for 12+ months

How will a looming recession affect consumers, automakers and the auto service industry?

Economists are only half-joking when they quip that we could be close to ‘talking ourselves into a recession.’ With an annual inflation rate over 8%, volatile stock markets, record-high gas prices, and rising interest rates, there are many factors that are dampening consumer sentiment in the United States.

An economic slowdown will impact nearly everyone, and each household will feel it differently. Although a recession by definition has not happened yet, there are indications that economic growth is slowing. Economists are taking note, and more than a few are sharing predictions. But when it comes to your money and lived experiences, how much do words matter? It’s a question worth pondering.

Recessions happen every four years on average

Diane Swonk is one of the most respected macroeconomists today, and this is what she had to say in a recent interview with PBS NewsHour. “I think the probability of recession is very high in the second half of the year and as we move into 2023. In fact, we’re forecasting what’s called a growth recession, which is when growth is not enough to hold unemployment down, and it continues to rise in 2023 to derail the inflation we have and get it back to being insignificant to most consumers.”

What happens to auto sales in a recession?

If a recession is knocking on our door, it’s wise to prepare as best we can. For most consumers, that means saving money and spending less. Discretionary spending, essentially spending by choice rather than by need, always plummets in a recession. For some (but not all) households, discretionary spending includes that shiny new car you’ve had your eye on. In a recession, auto sales decline significantly.

Just how bad could it get? New vehicle sales in the U.S. fell nearly 40 percent during the ‘Great Recession’ of 2008. 2020’s pandemic-driven recession was the shortest in history, lasting just two months. Even then, auto sales were down 15 percent compared to 2019.

Economic slowdowns affect the auto service and repair industry too, but the magnitude of impacts will depend on just how bad it gets. In most scenarios, the demand for auto service will stay fairly steady (as everyone needs occasional car maintenance). When the Great Recession put several million Americans out of work, the impact was significant and long-lasting, and enough to reduce the demand for auto maintenance for a few years.

The truth is, no one knows what the economy has in store over the next few years. Regardless, it would be wise to prepare for the worst while hoping for the best, even if that means putting off the purchase of your next vehicle. Our prediction is that a recession will be with us for 12+ months and that we’re already in the beginning stages of it.

Consumers will drive less

Consumers will continue to drive less as a result of changes in our ways of working post-pandemic. The “new normal” for consumers will be significantly fewer miles per year than in pre-pandemic years. In fact, we’ve already seen this trend showing up in national surveys of driving habits.

In late 2021, a survey from Hankook Tire found that just 36 percent of Americans drive every day. The statistic decreased by 12% over the course of 2021, and if the first five months of 2022 are any indication, a new host of factors (notably record gas prices) are likely to keep drivers off the road.

A recent article in Forbes highlighted the staying power of remote work. A third of workers feel more productive at home, and 36% of remote workers say they’d quit if they were forced back to the office. The nature of work in America has changed forever. Remote work may have a lasting impact on America’s driving habits, but it’s not enough to stop the post-pandemic traffic jam.

According to the U.S. Department of Transportation, travel on U.S. roads rose 11.2% in December 2021 compared with December 2020. The spike has resulted in a nearly full recovery in road traffic compared to 2019, with just 1% fewer miles being driven.

What about gas prices? Clearly, driving costs a lot more than it did last year. The national average is $4.59 per gallon nationwide. That is 50 percent higher than gas was at this time last year, according to AAA. Shockingly, hundreds of dollars in added fuel expenses each month isn’t keeping drivers at home.

Memorial Day weekend is expected to bring 37.9 million Americans to the road, according to Arrivalist. That’s more than the last pre-pandemic Memorial Day weekend. Will Americans continue to disregard the cost of fuel? Time will tell. Our prediction is that Americans will not return to their pre-pandemic driving habits.

Get the most when you sell your car.

Compare and choose multiple offers in minutes:

The car shortage will continue

Last year, 11 million cars were lost from production due to the worsening semiconductor chip shortage. Unfortunately, it doesn’t look like it’s getting any better. So far in 2022, 1.8 million cars have been removed from automaker production schedules. Over half a million of those cars were scheduled to be built in North America.

Automakers will continue to struggle to produce enough new vehicles to meet consumer demand. The ripple effects from lost production in 2021 and 2022 will permeate throughout 2023, 2024 and 2025. We should expect a shortage of quality used cars and prohibitively high prices for in-market car buyers. Used vehicles will continue to appreciate (or at a minimum not depreciate as they did in pre-pandemic times). We’ve seen used car prices rebounding yet again over the past few weeks (see the latest numbers here).

The average age of a vehicle on the road will continue to increase as consumers hold onto their existing cars longer. The average light-duty vehicle on American roads is now over 12 years old. Twenty years ago, the average auto was 9.6 years old. Drivers are responding to the car shortage by simply holding on to their cars longer. That’s not a bad idea with the way things are going. We expect this trend to continue.

Increased consumer demand for fuel efficiency (EV, PHEV and Hybrids)

Electric vehicle market share surpassed 5% for the first time in the first three months of 2022. And that was BEFORE gas prices shot up. But it’s not all about EVs, either. Hybrids, plug-in hybrids and full battery electric vehicles (collectively known as electrified vehicles) were up 41% year-over-year in 2021, despite average prices being thousands more than combustion engine counterparts.

Even as consumers drive less, we should expect to see continued and increased demand for EV and hybrid powertrain vehicles. More consumers will become EV and Hybrid “curious” and consider those powertrains for their next vehicle.

The average transaction price for a fully-electric vehicle is roughly $11,000 more than ICE vehicles. Incentives (such as the federal EV tax credit) help some buyers overcome the cost, but it’s still a luxury that most driver’s can’t afford. Will EVs get any cheaper? Not anytime soon, especially since battery production costs have thrown a wrench into automaker’s plans to lower prices.

Rising interest rates make borrowing more expensive

In an effort to mitigate inflation, we should expect interest rates to rise further. As the cost to borrow money increases, consumers (and businesses) will be more cash-conscious than before. The Federal Reserve just raised interest rates for the first time in three years, and they said it surely won’t be the last hike.

New car buyers probably won’t see much of a change at first. Captive lending makes it possible to hold off major rate increases for as long as possible to entice buyers into the dealer showrooms. However if the mortgage industry is any foreshadow of what’s to come, car buyers should expect auto interest rates to increase expeditiously over the coming months.

It’s important to remember that a higher interest rate will cost buyers of expensive vehicles most (on a dollar-for-dollar basis). A 6% interest rate will result in about $6,000 in total interest paid for a $40,000 loan over 60 months, but just $2,400 for a $15,000 loan over the same term.

How much do rising interest rates increase car payments? Let’s consider this example. Right now, the average amount borrowed with an auto loan is roughly $40,000 (wow!). With a 72-month loan, a 3.5% interest rate would result in $4,400 in interest paid over the life of the loan. With a 6% interest rate, that same loan would cost $7,700 in interest. It’s not pocket change.

CarEdge’s Take

Of our 5 predictions for 2022 and beyond we are most concerned about the impacts of a global recession and the continued car shortage. It’s impossibly difficult to predict all of the effects we’ll see from these phenomena, however we’re cautiously optimistic that we’ll be able to “weather the storm” and be on firmer footing because of it. By 2025 we think we are on the other side of “this”.

What can you do about these 5 known factors in the remainder of 2022? Stay alert, informed and prepared. Whether that means saving a few extra dollars or making that older vehicle last a little longer, every little bit will help ease the anxiety brought on by the uncertain times we live in.

Buying a car in 2022 is hard. Deciding if you should buy a new or used vehicle is even more difficult. Used car prices have increased unlike any other time in history, and the new car shortage means you may need to wait months to take delivery of an ordered vehicle.

While in years past the answer to “should I buy a new or used car” was more obvious, today it is trickier to answer. Let’s break down the pros and cons of buying new and used and what our recommendation is here at CarEdge.

Let’s dive in.

The case for buying a new car

You might feel a little crazy if you buy a new car in 2022 … Just a few years ago, the idea of paying MSRP for a new car was unheard of. Today, paying MSRP is a deal.

Car dealers nationwide have been adding additional dealer markups (ADMs) to their vehicles. For many brands, the average transaction price is well above the original vehicle’s MSRP.

If new cars are selling for more than MSRP, how could it possibly make sense to buy one in this market? The case is quite simple; if you can find a dealership who will sell you a vehicle at MSRP (and in some cases below it), then you should jump on it.

The 5 Most Marked-Up Cars in 2022

It is widely expected that automakers will significantly increase their MSRPs for the 2023 model year. We have already seen many manufacturers increase MSRPs during the 2022 model year.

Pair this with the reality that used vehicles are appreciating assets, and you can begin to see why purchasing a 2022 new vehicle at MSRP is a relative “bargain”. New vehicles come with the full manufacturer warranty and typically are eligible for special financing through the manufacturer’s lending arm. Used vehicles are selling for the same price as new vehicles and they don’t have those benefits. For this reason, if you can find a dealership selling a vehicle at MSRP we recommend you strongly consider it.

To find a dealership selling at MSRP we encourage you to search our community-driven dealership reviews. Research over 1,700 reviews that have been submitted by other community members.

Get the most when you sell your car.

Compare and choose multiple offers in minutes:

The case for buying a used car

What is the rationale for buying a used car in 2022? Price. If you cannot afford a new vehicle (which is understandable since the average transaction price in April 2022 was $42,000), then older used cars become your only option.

Sadly, 8-16 year old used cars have seen the most rapid price appreciation so far in 2022. This is because many people are looking for under $20,000 price-point vehicles and their only options are older used cars.

If you are looking for a vehicle in this price range it is critically important that you do your due diligence before purchasing it. Pre-purchase inspections are non-negotiable in today’s market. We have heard many horror stories of “junk” cars being sold to consumers, and the best way to protect yourself from that happening is to get an inspection done before you purchase.

Not all used cars have appreciated equally. Gas guzzler vehicles have depreciated in 2022, while compact and subcompact sedans have appreciated. The trade off here is obvious; save money by spending less on gas guzzler vehicle, but spend more on fuel, or spend more on a more fuel efficient smaller car and save on fuel.

Buying a used car in today’s market is incredibly challenging.

Should I buy a new or used car — why we recommend new

If you’re reading this blog post, the odds are high that you already knew it is a tough time to buy a new or used car. Unlike in years past where the financially prudent decision was to buy a used car, we think it makes more sense to buy a new vehicle in 2022. While that’s easier said than done, we think it will pay off in the long run.

If you cannot afford a new vehicle, then finding a used vehicle that passes a pre-purchase inspection is your best bet.

As always we recommend going through Deal School before you contact any seller, and please don’t hesitate to post on the free community forum to get help. It’s a challenging market, but we’re here to help.

October 2022 Update: Hyundai and Kia models with dual-clutch transmissions are subject to a new recall and stop-sale. Model year 2021 – 2023 vehicles are included. See the details below.

A recall remains in effect for the Kia Telluride and Hyundai Palisade. This recall is separate from another recall earlier this year in which nearly 6 million vehicles produced between 2011 and 2019 were flagged for separate fire risks. See the details and learn how to check if your VIN number is included below.

Let’s dive in to what you need to know about Kia & Hyundai fire recalls.

What Kias & Hyundais are being recalled for fire?

NHTSA Recall ID

Vehicle Make

Vehicle Model(s)

# Vehicles Recalled

Recall Date

21V331

KIA

2013-15 Optima and 2014-15 Sorento

440,270

5/10/2021

21V308

HYUNDAI

2021 Santa Fe

2

5/3/2021

21V301

HYUNDAI

2019-20 Elantra, 2019-21 Kona and Veloster

125,840

4/28/2021

21V303

HYUNDAI

2013-15 Santa Fe Sport

151,205

4/28/2021

21V277

KIA

2022 Kia Carnival

2,744

4/21/2021

21V259

KIA

2021 Seltos, 2020-21 Soul

147,249

4/13/2021

21V208

HYUNDAI

2021 Genesis G80, GV80

147

3/25/2021

21V160

HYUNDAI

2015-16 Genesis, 2017-2020 Genesis G80

94,646

3/10/2021

21V161

HYUNDAI

2019-21 Genesis G70

552

3/10/2021

21V137

KIA

2017-19 Cadenza, 2017-21 Sportage

379,931

3/4/2021

20V750

KIA

2012-2013 Sorento, 2012-2015 Forte and Forte Koup, 2011-2013 Optima, Hybrid, 2014-2015 Soul, and 2012 Sportage

294,756

12/2/2020

20V746

HYUNDAI

2012 Santa Fe, 2011-13 and 2016 Sonata Hybrid, 2015-16 Veloster

128,948

12/1/2020

20V630

HYUNDAI

2019-2020 Kona

6,707

10/13/2020

20V543

HYUNDAI

2016-2021 Tucson

652,054

9/4/2020

20V518

KIA

2019 Stinger

9,443

8/27/2020

20V519

KIA

2013-15 Optima and 2014-15 Sorento

440,370

8/27/2020

20V520

HYUNDAI

2013-15 Santa Fe Sport

151,205

8/27/2020

20V399

KIA

2020 Sedona

5,385

7/8/2020

20V393

HYUNDAI

2011-2012 Elantra and Sonata Hybrid, 2012 Accent and Veloster

Hyundai and Kia owners began suing the automakers in 2015 after they refused to pay to repair or replace the Theta II engine. Hyundai settled the class-action suit.

What is this lawsuit about? The people who filed these lawsuits are called Plaintiffs, and the companies they sued, HMA, HMC, and others, are called Defendants. The Plaintiffs allege that the Class Vehicles suffer from a defect that can cause engine seizure, stalling, engine failure, and engine fire. They also allege that engine seizure or stalling can be dangerous if experienced. Furthermore, the Plaintiffs also allege that some owners and lessees have been improperly denied repairs under the vehicle’s warranty. HMA and HMC deny Plaintiffs’ allegations.

Which Hyundai vehicles are included? The “Class Vehicles” are 2011–2019 model year Hyundai Sonata, 2013–2019 model year Hyundai Santa Fe Sport, and 2014–2015 and 2018–2019 model year Hyundai Tucson equipped with 2.0 liter and 2.4 liter genuine Theta II gasoline direct injection engines within OEM specifications.

What can I get from the settlement?

Warranty Extension

Reimbursement for Past Repairs

Reimbursement for Rental Car, Towing, Etc.

Compensation for Inconvenience Due to Repair Delays

Compensation If You Traded In or Sold a Class Vehicle

Compensation for Vehicle Involved in an Engine Fire

Rebate Program

2020-2022 Hyundai Palisade Recall

On August 22, 2022, the NHTSA issued a recall and stop-sale for model year 2020-2022 Hyundai Palisades in the United States. 245,030 Palisades are impacted. Affected new Palisades will not be available for purchase until they have received the recall fix.

The recall is due to a newly discovered fire risk that has resulted in three fires in Canada, and several instances of melted components.

A safety report filed with the NHTSA explains that debris and moisture accumulation on the tow hitch harness module printed circuit board may cause an electrical short, which can result in a fire.

On August 22, 2022, the NHTSA also issued a recall and stop-sale for model year 2020-2022 Kia Tellurides in the United States. 36,417 Kia Telluride VIN numbers are impacted. The stop-sale means that affected new Tellurides will not be available for purchase until they have received the recall fix.

Just as with the Hyundai Palisade recall, the Telluride recall is due to a newly discovered fire risk that has resulted in three fires in Canada, and several instances of melted components.

A safety report filed with the NHTSA earlier this month explains the risk of concern. Debris and moisture accumulation on the tow hitch circuit board may cause an electrical short. If a short occurs, accumulated debris may ignite and cause a fire.

One of the most common questions we get asked at CarEdge is, “What’s better right now, buying vs. leasing a car?” In 2022, with car prices going crazy, this question has become even more important to answer. In this article we’ll answer a few of the most common questions when it comes to buying vs. leasing a car. You’ll learn things like:

Is it cheaper to buy or lease a car?

What are the advantages of leasing versus buying?

What car should I lease?

Let’s dive in.

Buying vs. leasing a car in 2022

Depending on who you talk to, leasing is either the best thing since sliced bread, or a foolish financial mistake. Many people misunderstand what leasing is; it’s simply a contract between you and a third party company that allows you to rent an asset for a set period of time with pre-negotiated terms and conditions. It’s nothing more and nothing lease less.

When you lease a vehicle there are four important factors that make up your monthly payment:

When you lease a vehicle you do not purchase it, instead you are renting it. Instead of negotiating an out-the-door price (which is the price of the vehicle plus all taxes and fees), you negotiate the capitalized cost (also referred to as the “cap cost”) of the lease. The cap cost is the amount that is being financed with a lease. This will include:

The cap cost plays a major role in your monthly lease payment. As a rule of thumb, for every $1,000 in additional cap cost, that will roughly translate to $20 a month in payment on a 36 month lease. So if the salesperson won’t budge on their $2,000 paint and fabric protection package, that will end up costing you about $40 a month for three years. Ouch. With a lease you always negotiate the cap cost.

Get the most when you sell your car.

Compare and choose multiple offers in minutes:

Residual value

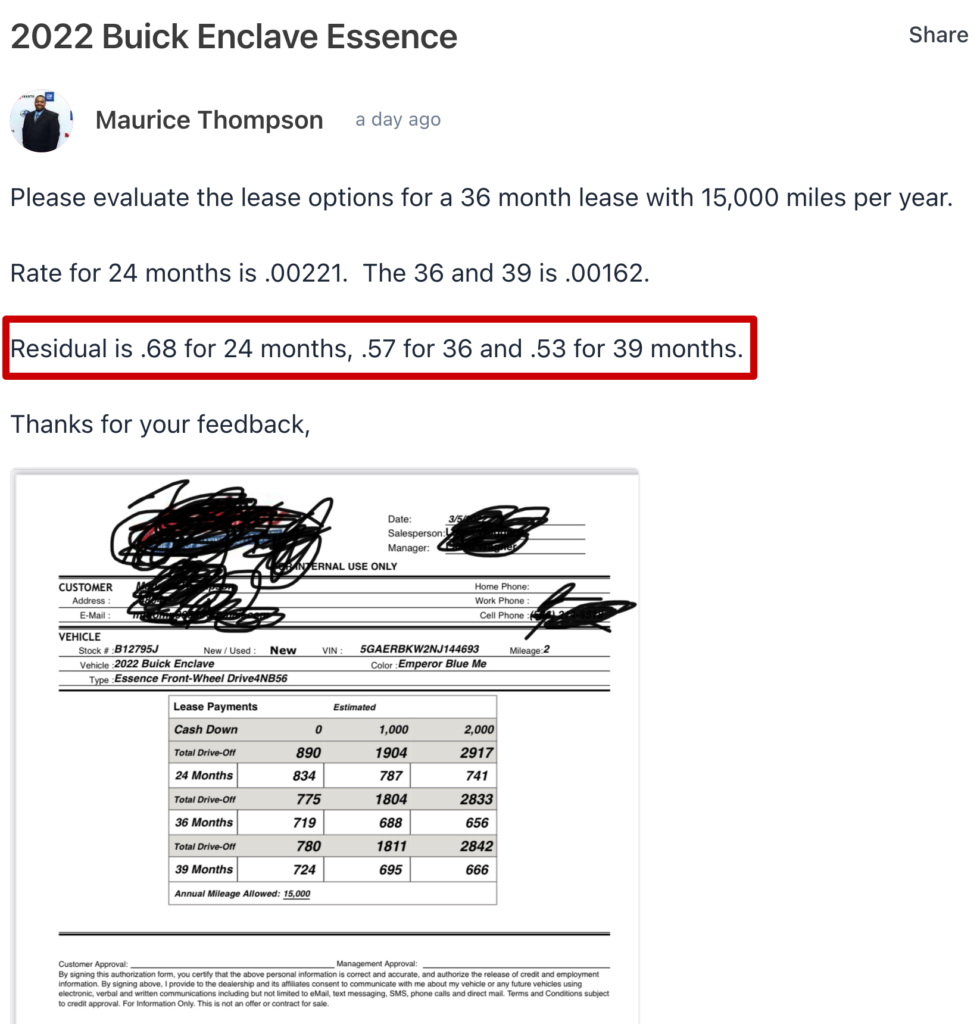

The residual value is the pre-set value that the leasing company says a vehicle will be worth at the end of the lease term. Residual values are represented as percentages of a vehicle’s MSRP, not the negotiated capitalized cost.

For example, in this car deal you can see that the dealer provided Maurice with three different residual values for three different lease term lengths.

When you lease, you pay for the amount of depreciation that will occur over the course of the lease term. In Maurice’s case if he leased for 24 months the residual value is 68%, which means he will have paid for 32% of the vehicle’s depreciation from MSRP.

👉 Residual values are not negotiable and they are set by the leasing company. Dealer’s cannot modify residual values.

Money Factor

The money factor is the interest rate on a lease. Instead of paying an APR on a loan, you pay a money factor on the lease. Money factors are typically expressed in decimals which can be confusing. Don’t fret. Ask the salesperson for the money factor and then multiply it by 2400, that’s the interest rate you are paying on the lease.

Why do you pay interest on the lease? Because the leasing company is financing the purchase of the vehicle from the dealer. They then turn around and lease the vehicle they just bought to you. To make money they charge the dealer an interest rate (the money factor) to cover their cost of financing the purchase of the vehicle. That then gets passed on to you, the customer.

Money factors can and will be marked up. That means the leasing company may charge the dealer .00125 (3%) for the lease, and the dealer will turn around and tell you the money factor is actually .00175 (4.2%). That’s a sizable difference in rate, and represents a large profit center for dealers on a lease.

👉 You can and should negotiate the money factor on a lease.

Sales tax

Most states charge sales tax on each lease payment, some states do not. NY, NJ, MN, OH, GA for example charge sales tax upfront on the total amount of the lease payments. VA, MD, TX charge sales tax on the total selling price of the vehicle (the cap cost). In all other states, sales tax is simply factored into your monthly payment.

Sales tax is not negotiable.

Okay, so those are the mechanics of leasing, but that doesn’t answer the question, “What’s better right now, buying vs. leasing a car?” We’ll answer that below.

Is it cheaper to buy or lease a car?

As we discussed above, there are four factors that impact how “good” a lease deal is. So far in 2022 we’ve seen two phenomena that make leasing less attractive than in prior years:

Residual values are low

Money factors are high

Since you can’t negotiate the residual value, there are some vehicles that are truly “unleasable” right now. Imagine leasing a Hyundai Kona EV for 36 months and paying for 50% of the vehicle’s depreciation. No thank you!

In most cases right now it is cheaper to buy instead of lease. That being said, there are still some advantages to leasing.

What are the advantages of leasing versus buying?

Proponents of leasing love to tout the benefits of not owning a car. When you lease there are three primary benefits:

You’ll have no negative equity at the end of the lease term

You’ll always be in a new car

If you want to buy your leased car at the end, you know the exact price you’ll pay, and you know how the car’s been driven and its maintenance and repair history

Since a lease is simply a rental, you’ll have no negative equity at the end of the term. Plus, with a lease you are committed for 3 years and then you can switch into something new. And, if you do chose to buy your lease car you know the vehicle history and shouldn’t have any concerns.

These are benefits of leasing no matter how good or bad the lease deal was.

What car should I lease?

So what cars actually lease well right now in 2022? If you’re seriously weighing buying vs. leasing a car, you should consider these vehicle’s as lease options:

Term

Year

Make

Model

MSRP

Average Payment (12,000 miles)

36

2021

BMW

i3

$48,970.00

$425.80

36

2022

KIA

NIRO EV

$43,495.00

$395.91

36

2022

CHEVROLET

BOLT EV

$33,595.00

$312.82

36

2022

CHEVROLET

BOLT EUV

$36,245.00

$341.01

36

2021

CHEVROLET

BOLT EV

$38,567.00

$367.63

36

2021

HONDA

CIVIC TYPE R

$41,940.00

$409.78

36

2022

TOYOTA

TACOMA

$36,323.33

$361.42

36

2022

TOYOTA

TUNDRA 4WD

$51,455.00

$524.43

36

2022

HYUNDAI

KONA EV

$39,435.00

$401.39

36

2022

MITSUBISHI

OUTLANDER PHEV

$40,356.67

$412.84

36

2021

POLESTAR

POLESTAR 2

$61,200.00

$623.95

36

2022

KIA

NIRO PLUG-IN HYBRID

$34,331.67

$350.88

36

2022

JEEP

WRANGLER UNLIMITED

$47,838.86

$502.42

36

2021

TOYOTA

TACOMA

$35,835.61

$378.09

36

2022

TOYOTA

TUNDRA 2WD

$48,478.57

$527.23

I need help with my car lease

Do you still have questions on buying vs. leasing a car? Get help from CarEdge’s team of car buying coaches. Click here to join CarEdge and get connected with a car lease expert who can help you navigate your deal. Here are some additional resources on car leases as well:

We receive a lot of questions here at CarEdge, and one has been more frequent than others recently, “Are car prices going down?” That question has flooded our email inbox, community forum, and YouTube video comment section. The answer is: YES.

Both new and used car prices are finally coming back to “normal,” although they have a long way to go. In this article we’ll update you on both new and used car prices, and give you some guidance on how to negotiate the best price if you need to buy a car.

Let’s dive in.

Are car prices going down?

Again, the short is an emphatic “YES.” Both new and used car prices have dropped in 2022. Let’s get into the nitty gritty of how much they’ve fallen.

New Car Prices

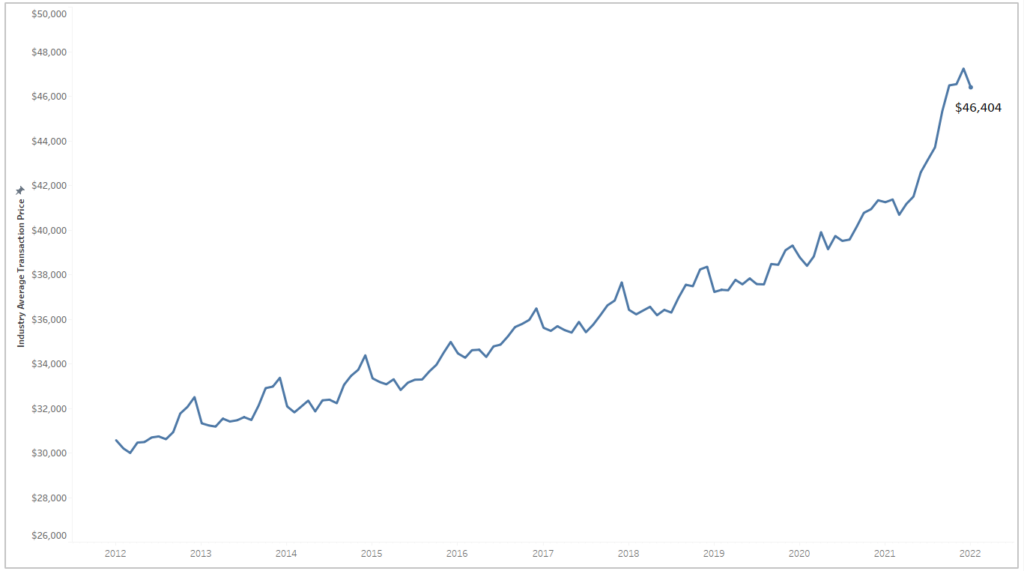

The average new car transaction price decreased in January 2022

New car prices have cooled off in 2022. After hitting a record high average transaction price of $47,243 in December of 2021, the average new car transaction price fell to $46,404 in January 2022.

Cox Automotive produces a new car “affordability index”, and that has declined as well. While the average new car price declined, interest rates jumped 17 basis points higher. As a result, the typical monthly payment for a new car declined 0.8% to $685 from what had been a record high of $690 in December.

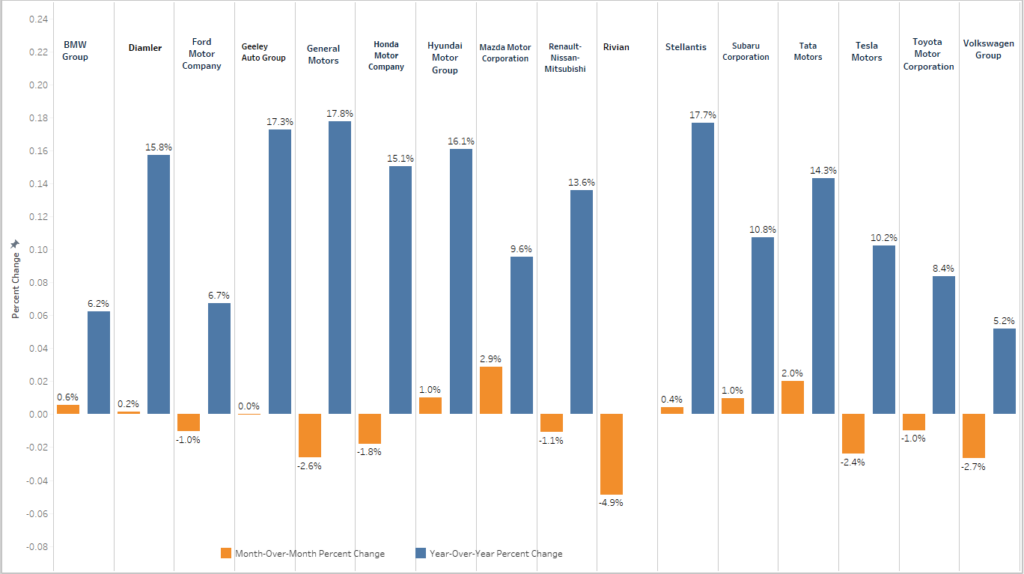

Not every automaker’s prices are going down at the same rate. Mazda prices have continued to climb month-over-month, while other automakers, like General Motors, Honda, and Volkswagen have seen their new car prices decline.

Used Car Prices

Are used car prices going down too? Yes, they absolutely are.

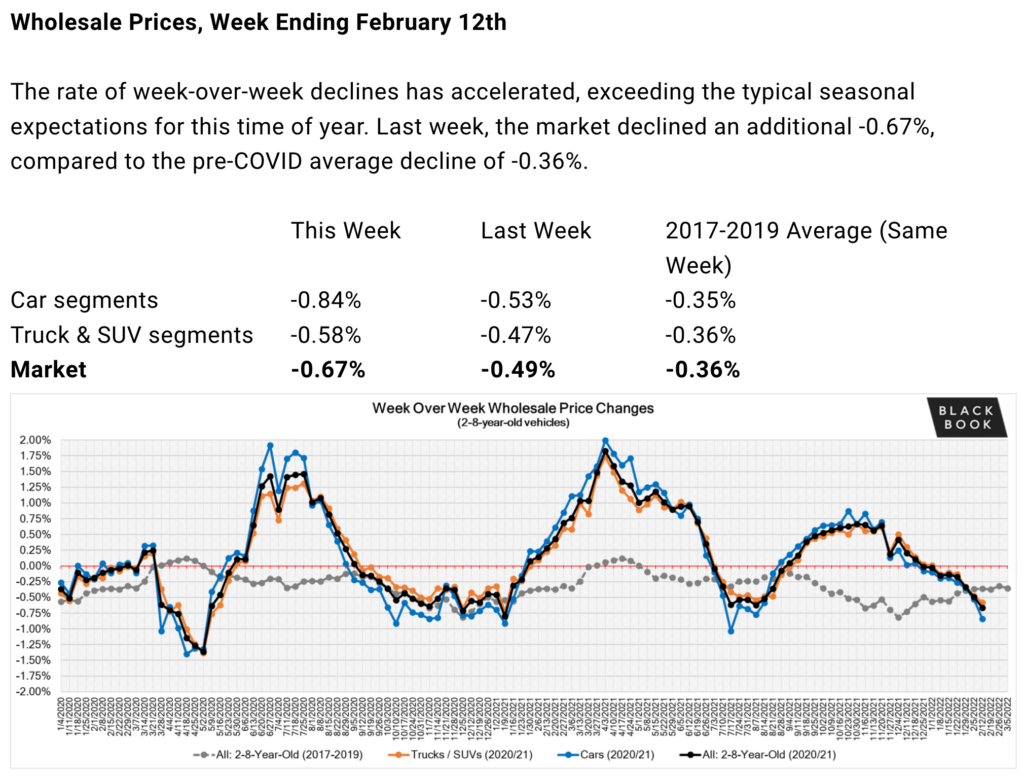

With used cars it is important to remember that there are two prices; the wholesale price, and the retail price. So far in 2022 we have seen both wholesale and retail prices go down.

Wholesale used car prices have dropped about 5%. Retail used car prices have stayed about flat, however dealers are once again negotiating and discounting used cars if you know how to do it.

Get the most when you sell your car.

Compare and choose multiple offers in minutes:

Wholesale prices have decreased more rapidly than retail prices. From Black Book you can see that the week-over-week depreciation of used cars has increased more rapidly then previously expected. This is a good thing for prospective used car buyers!

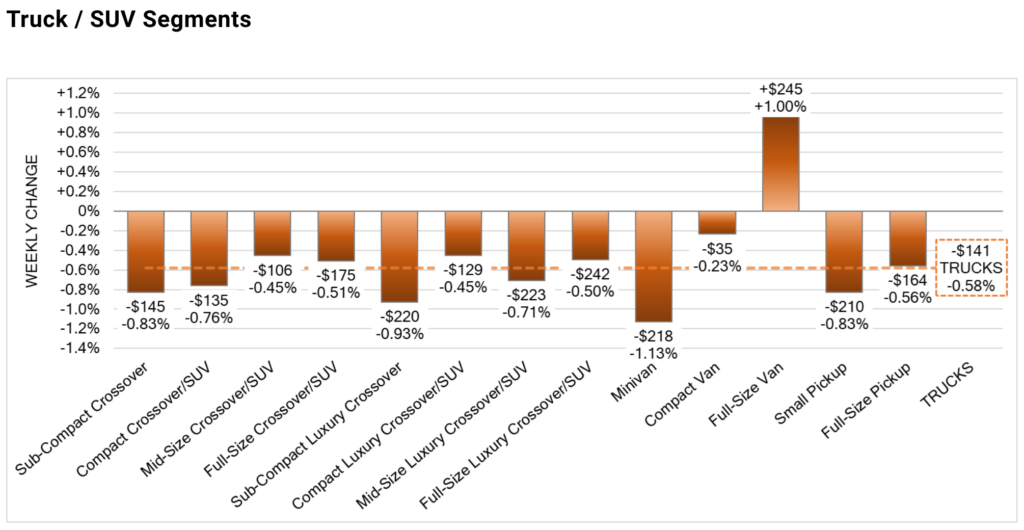

Not all used cars are the same however. For example, full-size vans continue to appreciate week-over-week.

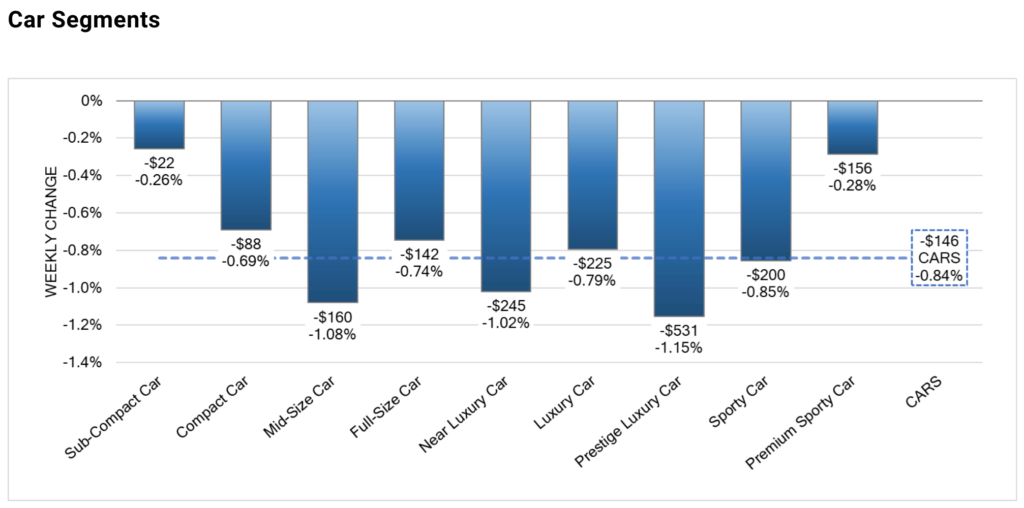

All segments of cars are declining in value week-over-week.

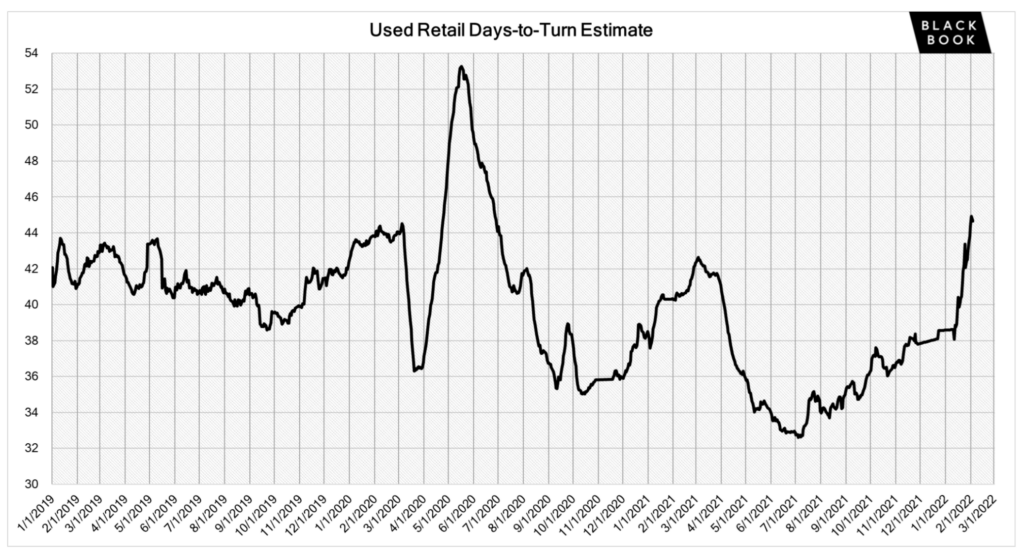

One of the most important indicators we analyze when assessing the used car market is “days to turn”. This is an industry metric that dealership’s measure to track their inventory. Car dealers do not pay cash for their inventory, instead they “floor plan” it. Just like you or I, the dealership finances the purchase of their inventory, and this means they pay interest on it each day it sits on the lot. A car dealer is more likely to negotiate on an “aged unit” (a car that has been on the lot for a while) than a brand new one, because the aged one has cut into their profit margin.

With all that in mind, data from Black Book shows that the number of days to “turn” (sell) a used car has increased dramatically. Pair this with rising interest rates, and you can quickly begin to see why dealers would be willing to negotiate on used cars once again.

When will car prices go back to normal?

While the most common question we receive is “are car prices going down,” the second most popular question is “when will car prices go back to normal?” The hard part about answering this question is that no one has a crystal ball, and it’s impossible to know just how bad the ongoing chip shortage still is.

That being said, it is obvious that consumer demand for new and used cars has softened. As a result, our expectation is that car prices will continue to go down in 2022, with a potential increase around tax return season (March and April). When will car prices go back to “normal” though is tough to say. Sadly, we think the new normal will be a world where new and used car prices are inflated relative to years past (2019).

New and used car prices may never return to 2019 levels. We feel this is particularly true on the new car side, since manufacturers have realized they do not need to spend as much money on incentives to sell their cars. Why would they ever discount like they did before if consumers continue to purchase?

Used car prices have a better chance of declining back to pre-pandemic levels, however you have to remember that used car prices increased over 40% in 2021, so it’s unlikely they will fall that much in a short period of time.

Is it a good time to buy a car?

This brings us to the third and final frequently asked question we receive, “Is it a good time to buy a car?” The answer is still, NO! Unless you absolutely need to buy a car, now is not a good time to buy one. Prices are still very inflated and incentives are few and far between. That being said, if you need to buy a car, now is a good time to do it.

The future is uncertain, and right now we do see CarEdge members getting factory order deals well under MSRP, as well as used car deals thousands of dollars below their advertised price.

States eligibile for below invoice pricing and 100% free delivery:

Alabama, Arkansas, Texas, Oklahoma, Florida, Georgia, Kentucky, Louisiana, Maryland, Delaware, Mississippi, North Carolina, South Carolina, Tennessee, Virginia, and West Virginia.

What if I don’t live in these states? If you're outside these areas, don't worry! We're committed to making sure everyone can enjoy our deals. Although the delivery fee will not be waived, you can still purchase from CarEdge and either pay for shipping or coordinate pickup at a participating dealer.

Getting Started!

Please enter the following information to generate a price-transparent price quote.

FAQ

How much does it cost?

Our concierge service costs $999 plus an optional shipping fee (based on distance or pick-up).

To get started, pay a 50% deposit and a CarEdge team member will contact you within 24 hours.

Why should you let a concierge do the work?

Get the best deal

Our team of concierges and industry experts with 75+ years of combined experience with access to tools and data to leverage the best deal possible.

Convenience

Gone are the days of looking for a car and stepping into the dealership spending hours and hours of head banging only to get smooth talked into a higher price.

Expert assistance

We answer all questions you may have regarding the buying process, what the right car is, the deal itself, and more!

Who are the concierges?

Transparent when others aren't

Our commitment to transparency and honesty ensures that you make informed decisions, while our years of experience guarantee that we will be able to secure the best deal for you.

When you win, we win

We work for you, not the dealership, ensuring your interests are always our top priority.